Managing education expenses demands foresight and realistic planning. Families and learners face changing costs across stages of study and life.

This guide outlines a stepwise approach to estimate costs and build flexibility into funding. It focuses on clear milestones, practical savings, and adaptable plans rather than one-size-fits-all solutions.

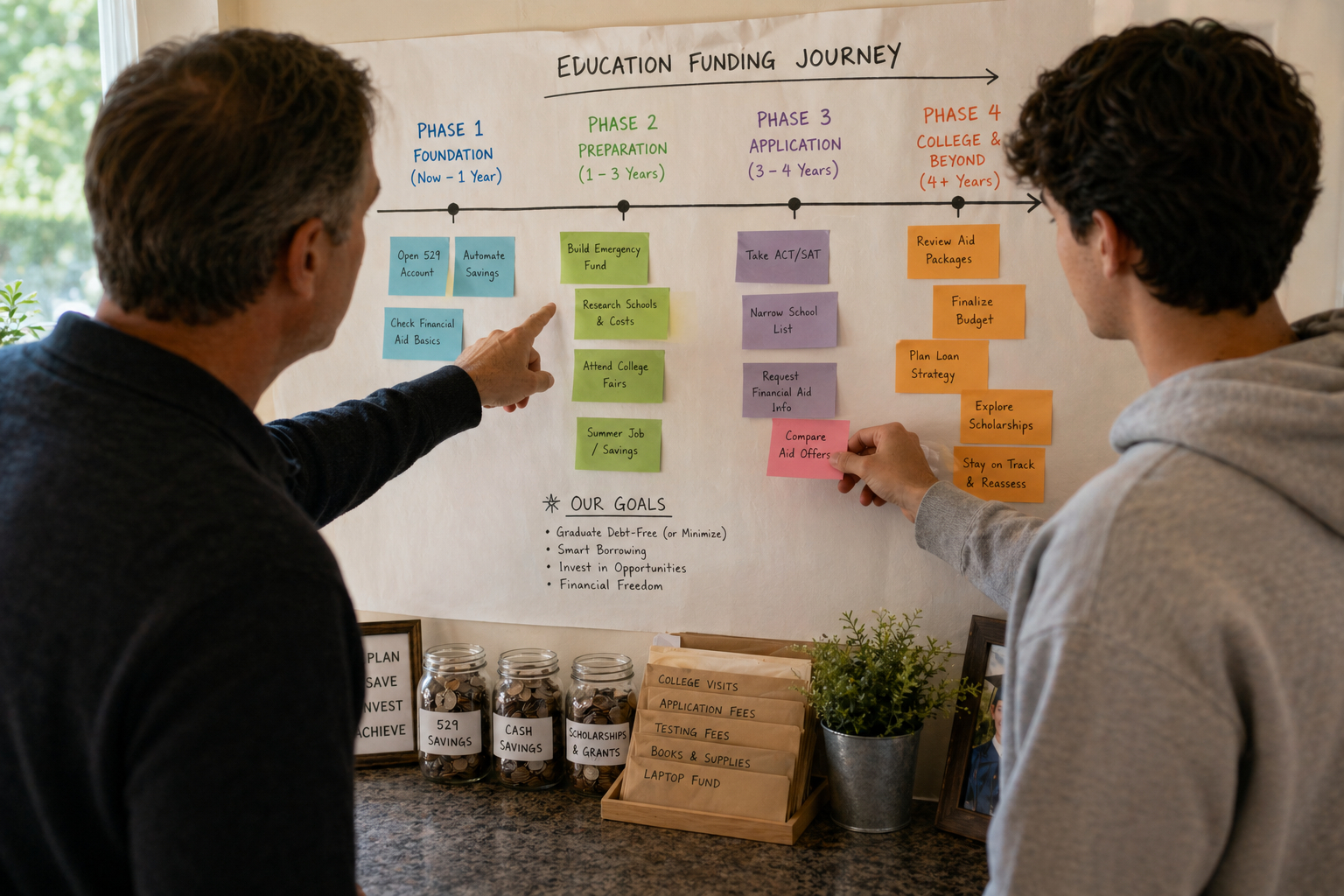

Assessing True Education Costs

Start by mapping anticipated expenses across each stage, including fees, materials, and ancillary costs. Factor in inflation, possible program changes, and non-tuition expenses such as housing and transport. Estimate ranges rather than single figures to capture uncertainty and create upper and lower scenarios.

Document assumptions so projections can be reviewed and updated as circumstances change.

A transparent cost map helps prioritize which expenses require dedicated savings and which might be deferred or reduced.

This clarity guides realistic target setting.

Prioritizing and Phasing Expenses

Break goals into milestones—preparatory, enrolled, and graduation or certification phases—and assign timing to each. Prioritize mandatory costs first, then high-impact enhancements like tutoring or specialized equipment. Phasing allows families to allocate resources in manageable increments and reduces pressure on cash flow.

Use timelines to sync savings, financial aid applications, and part-time income opportunities.

Regularly revisit priorities as academic plans evolve. Flexibility in sequencing can lower overall cost stress.

Practical Savings and Funding Options

Combine predictable savings vehicles with contingency buffers to cover unexpected expenses. Explore scholarships, grants, employer support, and low-cost alternatives where available, aiming to minimize reliance on debt. Short-term accounts that remain accessible near spending dates limit penalties and market risk.

Consider matched savings or goal-specific accounts when possible to reinforce discipline.

- Scholarships and grants

- Part-time work and apprenticeships

- Goal-specific savings accounts or funds

A diversified approach reduces single-point failures in funding. Document each source and its conditions so you can activate it when needed.

Preparing for Unplanned Expenses

Despite careful planning, unplanned costs can appear—illness, program changes, or travel may add unexpected bills. Maintain an emergency buffer equivalent to a small term of tuition or living expenses to absorb shocks without derailing goals. Consider short-term insurance, refundable options when booking, and flexible vendors who allow rescheduling. When a shock occurs, reassess nonessential contributions and prioritize immediate obligations.

Transparent communication with family members and educational institutions can unlock short-term support or fee adjustments. A prepared buffer preserves momentum toward long-term education objectives.

Monitoring and Adjusting Your Plan

Set regular review points—annual or per academic year—to compare projections against reality and adjust contributions. Track expenses in simple spreadsheets or budgeting apps and flag variances early. When income or costs shift, rephase noncritical spending and explore additional support options. Small, frequent adjustments prevent surprises and keep the plan realistic.

A living plan is more effective than a perfect initial projection. Stay pragmatic and keep communication open among stakeholders.

Conclusion

Forecasting and funding education costs is an ongoing, adaptable process. By mapping expenses, prioritizing milestones, and combining savings with diverse funding, families can reduce uncertainty. Regular reviews and small adjustments keep plans aligned with changing needs.