Education expenses can shift unexpectedly, creating strain on household plans. A proactive approach reduces stress and keeps goals on track over time. This article outlines practical steps to forecast, budget, and adapt funding strategies. Readers will find actionable tactics that fit different income patterns and learning stages.

Assess Costs and Forecast

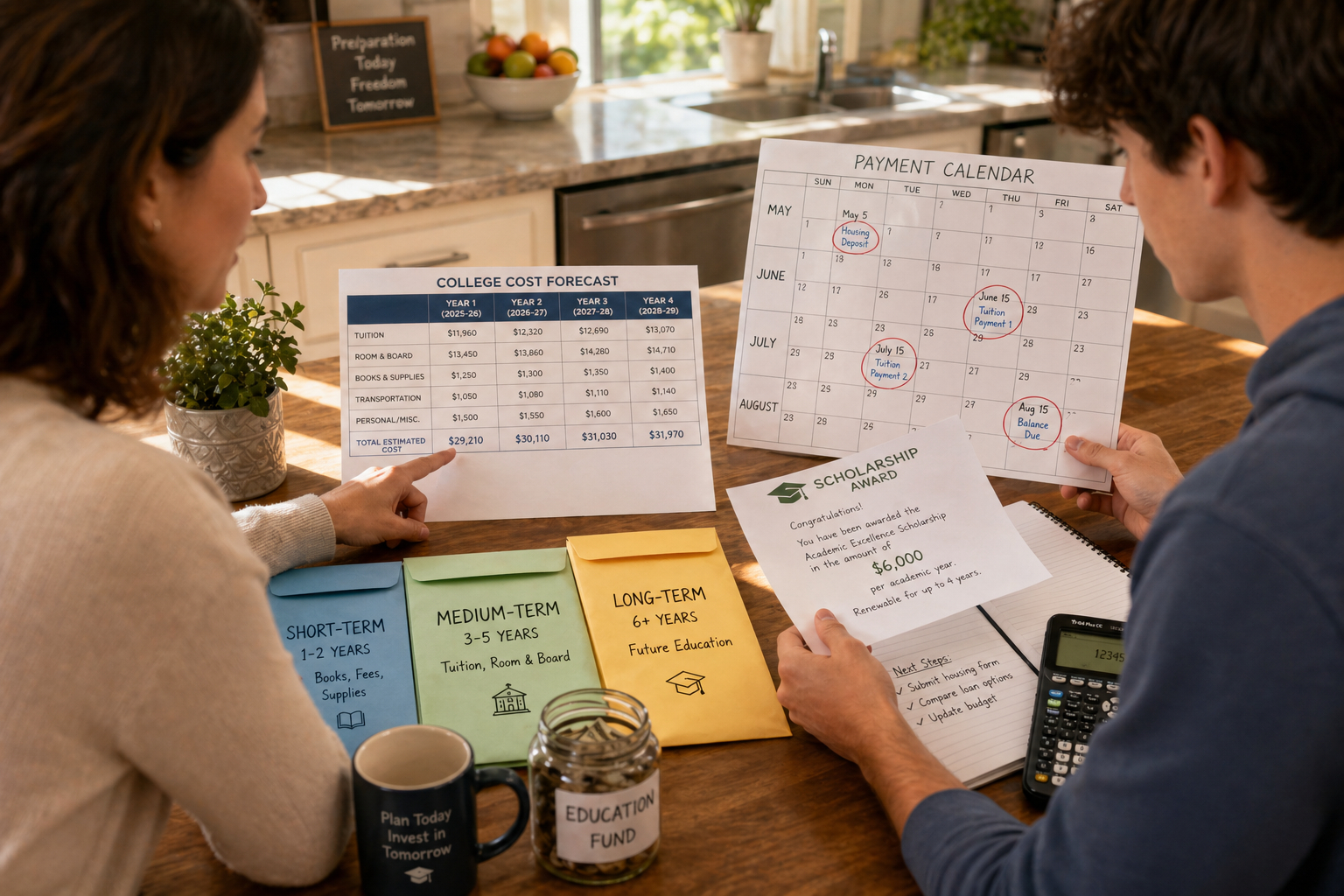

Begin by mapping realistic costs for each stage of learning, including tuition, materials, and living expenses. Use conservative assumptions about price increases and consider multiple scenarios to reveal potential shortfalls. Regularly update these forecasts as choices and circumstances change, and include timing for payments so cash flow needs are clear. Account for indirect costs such as technology upgrades, travel, and credentialing fees to avoid surprises.

Document assumptions and revisit them annually or when major decisions arise. Transparent forecasting makes tradeoffs easier to evaluate and supports better conversations with family or stakeholders. Keeping a simple version of the forecast accessible improves responsiveness when plans shift.

Create Flexible Saving and Funding Tiers

Design a tiered funding approach that separates short-term, medium-term, and long-term needs. Keep some funds in liquid accounts for imminent costs while allocating longer horizon savings to vehicles that match risk tolerance. Combine scholarships, targeted savings, and predictable income sources so no single element must cover all risk. Consider matching options, employer benefits, and phased payment plans when shaping each tier.

- Short-term: emergency and upcoming semester fees.

- Medium-term: targeted savings for program-specific expenses.

- Long-term: investment accounts for major degree costs and planned tuition increases.

These tiers help align timing with liquidity and expected returns. Rebalancing between tiers prevents misallocation when circumstances shift. A written funding policy for the household makes allocation decisions repeatable and less stressful.

Manage Cash Flow and Contingencies

Build a cash-flow plan that layers income, scholarships, work-study, and savings to cover regular outflows. Identify potential contingency sources such as flexible loans, short-term lines of credit, or employer reimbursement programs before emergencies occur. Reducing nonessential spending during high-cost periods preserves the ability to cover core education expenses and minimizes high-cost borrowing. Track upcoming billing dates and align pay periods with key payments to smooth monthly pressure.

Establish simple triggers to pause discretionary spending and tap contingency funds. Clear rules make responses timely and reduce stress during unexpected events. Periodic drills—reviewing how the plan performs under a simulated shock—reveal weak points and build confidence.

Review, Adjust, and Communicate

Set regular check-ins to compare actual spending against forecasts and adjust contributions as needed. Open communication between family members or funding partners about priorities and tradeoffs prevents misaligned expectations and last-minute surprises. Use technology tools or shared documents to keep records current and accessible to those involved. Adjust timelines or program choices when cost-benefit analysis indicates a better path.

Continuous review creates a culture of informed decisions rather than reactive measures. When everyone understands the plan, it becomes easier to make consistent choices and protect the most important educational goals.

Conclusion

A practical, layered approach turns unpredictable education costs into manageable decisions. Forecasting, tiered funding, and clear cash-flow rules provide flexibility and clarity. Small, regular updates keep plans resilient as circumstances change.