Rising education expenses are a common concern for students and families planning for the future. Finding ways to stretch a budget while maintaining academic quality requires deliberate planning and informed choices. This article outlines practical steps that help control tuition, living costs, and related expenses without compromising outcomes. By combining assessment, aid optimization, and smart decisions, you can reduce financial strain and keep focus on learning.

Assess Your True Education Costs

Start by creating a detailed budget that includes not only tuition but also fees, textbooks, housing, transportation, and daily living expenses. Tracking monthly cash flow helps reveal hidden costs like parking permits, lab fees, or subscription services that add up over time. Compare projected costs across institutions or programs to identify where savings are realistic without lowering academic standards. Accurate assessment empowers better decisions when selecting courses, housing options, or part-time work schedules.

Knowing exact costs also improves conversations with financial aid offices and advisors. A clear budget makes it easier to prioritize needs and spot areas for immediate adjustment.

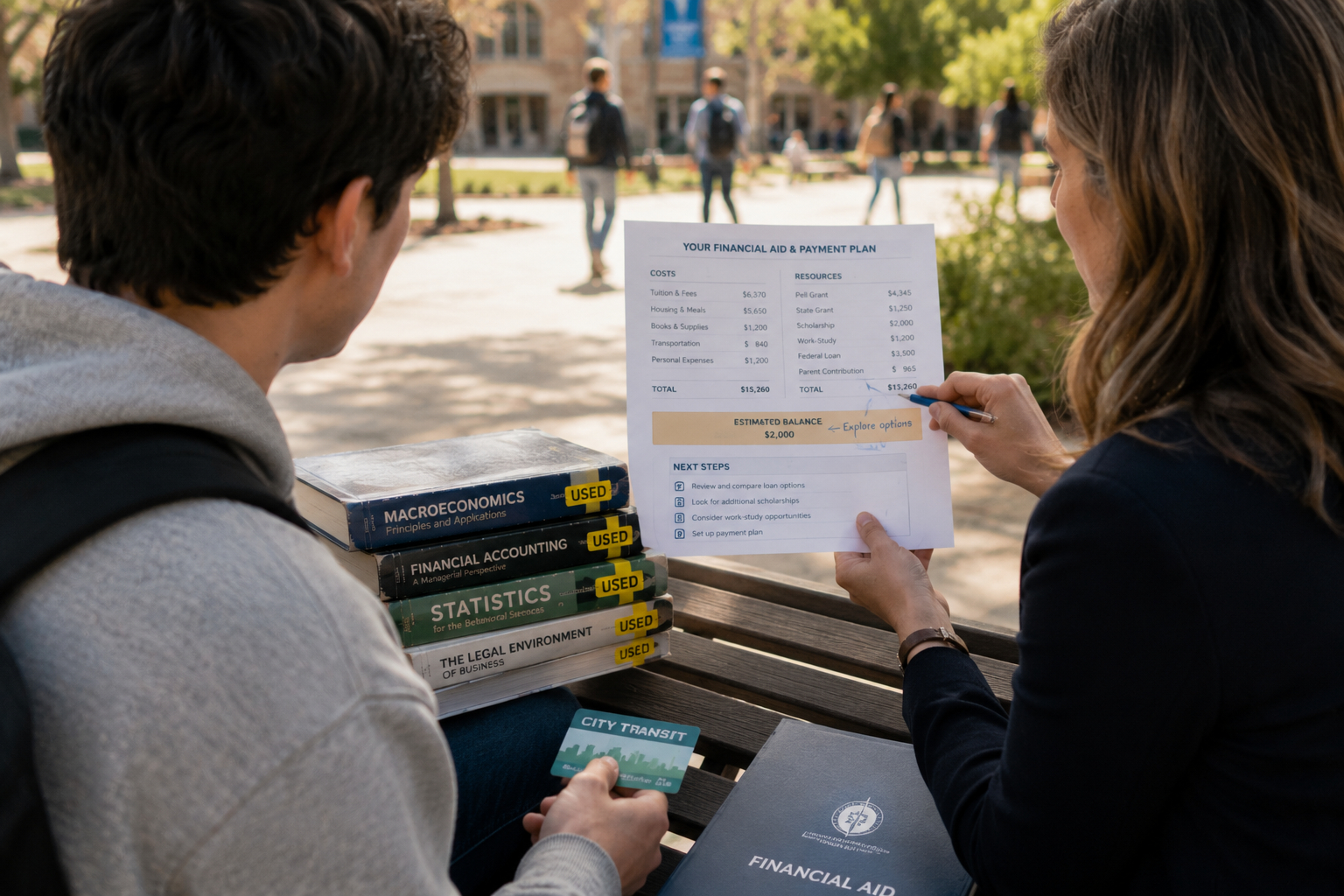

Maximize Aid, Scholarships, and Institutional Support

Explore all forms of financial aid early, including grants, scholarships, work-study, and institutional awards that do not require repayment. Use scholarship search engines, departmental opportunities, and community foundations, and remember that small awards can combine to make a significant difference. Complete the required financial forms on time and follow up with schools about available institutional discounts or payment plans. Don’t overlook employer tuition assistance or credit options that can lower net costs.

Applying broadly increases the chances of receiving non-loan support and reduces reliance on borrowing. Regularly revisit aid opportunities as your circumstances change.

Smart Cost-Saving Choices That Preserve Value

There are many ways to lower expenses while keeping the educational experience strong, such as taking general education credits at a lower-cost institution or choosing open educational resources over expensive textbooks. Consider part-time work, internships, or cooperative education that provide income and valuable experience, often offsetting costs. Online or hybrid courses can reduce commuting and housing expenses, but evaluate program quality and accreditation before committing. Buying used materials, sharing resources, and leveraging campus services like career centers all contribute to smarter spending.

Small, consistent changes often have more impact than drastic cuts. Prioritize options that maintain or enhance learning outcomes.

Plan for Long-Term Affordability

Think beyond immediate semesters to create a sustainable plan that limits debt and supports timely graduation. Set milestones for credit completion, monitor loan balances, and create an emergency fund to avoid high-interest borrowing. Regularly review and adjust the plan as financial aid, living situations, or academic goals evolve. Financial literacy and proactive communication with advisors help ensure the plan remains realistic and effective.

Long-term planning reduces stress and preserves flexibility when opportunities arise. A few intentional choices now can deliver ongoing benefits throughout a career.

Conclusion

Careful assessment, targeted aid strategies, and value-focused choices can significantly reduce education expenses. Combining short-term adjustments with long-term planning protects academic quality and limits debt. Adopting these practices helps students achieve goals without unnecessary financial sacrifice.